Organizing personal finances requires a clear, adaptable framework that keeps money aligned with life goals. The seven strategies below create a worldwide roadmap that withstands surprises and supports lasting prosperity.

1. Define Goals That Guide Every Decision

Clear goals transform abstract saving into purposeful action with measurable milestones.

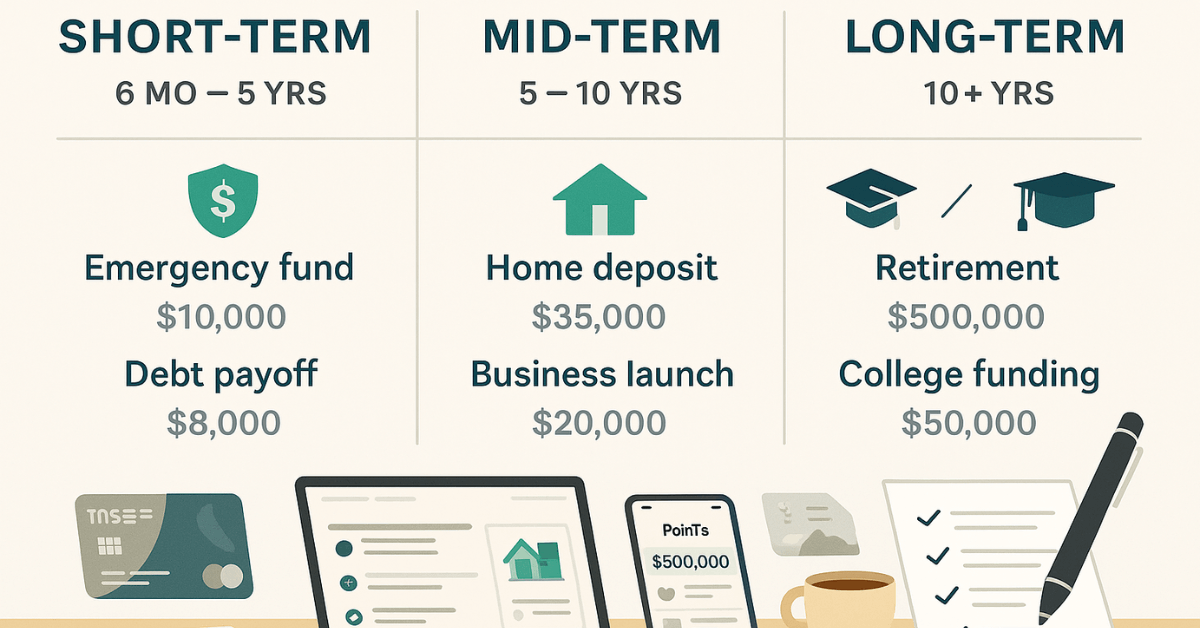

Start by envisioning the lifestyle you expect in five, ten, and twenty years — consider housing, travel, education, and retirement. Assign specific price tags and realistic deadlines to each dream. Segment objectives into three buckets:

- Short-term (six months – five years): building an emergency fund or finishing credit-card repayment.

- Mid-term (five – ten years): funding a home down payment or launching a business.

- Long-term (more than ten years): paying several years of college tuition or retiring early.

Classify each target as a need or want so priorities remain flexible when circumstances shift. A written list keeps motivation high and drives the steps that follow.

2. Track Cash Flow and Build a Sustainable Budget

A precise picture of income and expenses reveals hidden money you can redirect toward goals.

Record every source of take-home pay and every outgoing peso, dollar, or euro. Group spending into needs (housing, utilities, transportation), wants (entertainment, dining), and future (savings, debt repayment).

Many worldwide households favor the 50/30/20 guideline:

- 50 % Needs

- 30 % Wants

- 20 % Savings and Debt Reduction

Use banking apps, spreadsheets, or budgeting software to monitor progress daily. When outflows exceed targets, trim discretionary costs first or negotiate recurring bills. Consistent tracking prevents smoke-alarm moments and frees cash for the next tips.

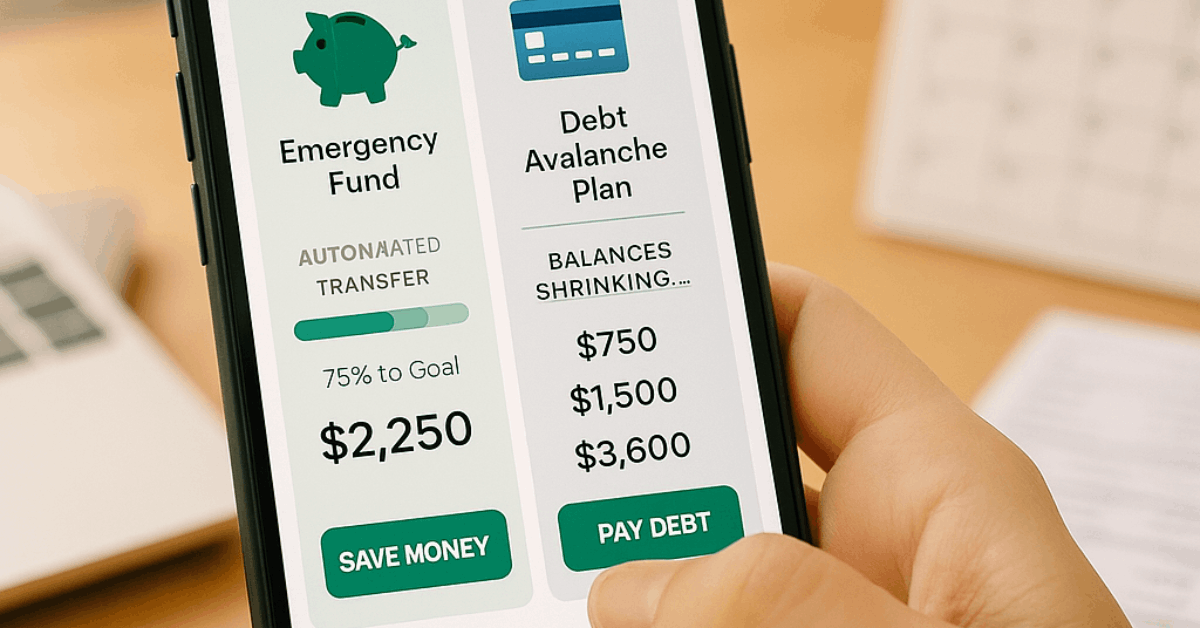

3. Establish an Emergency Cushion and Insurance Safety Net

Financial shocks are inevitable; a cushion and the right policies keep goals intact.

Begin by saving $500, then $1 000, and gradually reach one month of core living costs. Small automatic transfers make the habit painless.

Build credit while you save, as strong credit scores can lower borrowing costs when opportunities or crises arise. Protect the budget further with insurance that fits each stage of life:

- Renters' or homeowners' insurance guards belongings.

- Health and critical-illness coverage shields against medical bills.

- Term life insurance replaces income for dependents.

- Disability insurance safeguards earning power if illness or injury strikes.

Adequate coverage means an accident, layoff, or storm becomes a setback, not a derailment.

4. Eliminate High-Interest Debt Strategically

Debt with high interest rates—especially from credit cards—can quietly drain your financial potential. If left unchecked, interest charges grow faster than most investment returns, slowing your ability to build wealth or fund future goals.

Start by listing all current debts: include the outstanding balance, interest rate, minimum monthly payment, and payment due dates. This provides a comprehensive view of your obligations and helps identify the most expensive loans to target first.

Avalanche Method

This strategy focuses on minimizing total interest paid over time. You make the minimum payments on all debts but direct any extra money toward the account with the highest interest rate, regardless of the balance. Once that’s paid off, move on to the next-highest rate, and so on.

- Best for: People who are analytical, patient, and focused on financial efficiency.

- Why it works: You reduce the total amount of money lost to interest, accelerating your path to debt freedom.

Snowball Method

This method emphasizes psychological momentum. You pay the minimums on all accounts, but put any extra cash toward the smallest balance first. Once it's gone, you move to the next-smallest balance, creating a series of quick wins that build confidence and motivation.

- Best for: People who need encouragement to stay consistent or feel overwhelmed by debt.

- Why it works: You achieve early victories, which can make sticking with the plan emotionally easier, even if it takes slightly longer or incurs higher interest costs.

Consolidation and Repayment Plans

If your debt feels scattered or hard to manage, consider:

- Debt consolidation loans with lower interest rates allow you to combine multiple balances into one payment.

- Balance transfer credit cards offering 0% introductory rates—if used responsibly and paid off before the promo ends.

- Nonprofit debt-management programs negotiate reduced rates and structure a single monthly payment on your behalf.

Automate payments that exceed the minimum whenever possible. This removes reliance on willpower and ensures steady progress. Even a small recurring extra payment, such as $50, adds up over time.

Once high-interest debt is paid off, redirect the freed-up funds toward your long-term goals, such as investing, building an emergency fund, or enhancing your insurance coverage.

Every dollar previously lost to interest becomes a building block for lasting financial growth.

5. Invest Early and Diversify for Future Growth

Enroll in an employer retirement plan and contribute enough to capture the full match; that match is free money. Gradually raise contributions toward the 2025 IRS maximum of $23 500, plus any catch-up allowance if aged 50 or older.

Supplement workplace plans with traditional or Roth IRAs and, when possible, a low-cost brokerage account. Early investing exploits compounding: an eight-percent annual return on $1 20 000 saved over thirty years can exceed $1 46 million, while doubling annual savings for only fifteen years produces roughly half that figure.

Multiple asset classes — stocks, bonds, and perhaps real-estate funds — reduce volatility and improve consistency worldwide.

6. Optimize Taxes and Retirement Contributions

Check recent pay stubs against last year’s refund or tax bill. If refunds run large, adjust Form W-4 to keep more money during the year. Explore credits and deductions that reward education, energy upgrades, and dependent care.

Fund Health Savings Accounts or Flexible Spending Accounts when available; both lower taxable income while covering inevitable medical costs.

Stay current on contribution limits: $7 000 for IRAs in 2025 (or $8 000 at age 50 plus), and higher catch-up allowances between ages 60 – 63 under the Secure 2.0 Act. Coordinating taxes and savings prevents unnecessary government donations and brings retirement closer.

7. Review, Adjust, and Protect Long-Term Legacy

Mark an annual calendar date to revisit budgets, insurance, and investment allocations.

Trigger an extra review after major events such as marriage, childbirth, promotion, inheritance, or relocation. Update beneficiaries on retirement accounts and life policies, and draft or refresh a will, durable power of attorney, and health-care directive.

Estate planning is not reserved for the wealthy; it simply clarifies who manages finances and healthcare if incapacity occurs and how assets transfer afterward. That clarity spares loved ones stress and preserves wealth across generations.

Conclusion

Organizing your finances isn’t about perfection—it’s about consistency, clarity, and alignment with what matters most.

By applying these seven strategies, you create a system that adapts to life’s changes, protects against setbacks, and steadily moves you closer to long-term financial stability and personal freedom.