Managing everyday spending does not require complicated tactics.

Practical steps, consistent tracking, and clear priorities help you keep more cash in your pocket and build lasting financial strength worldwide.

Let's get started learning simple strategies for your daily expenses.

Map Your Cash Flow for Real Clarity

Grasping the exact size of incoming and outgoing money lays the groundwork for every other decision.

Write down each expense, payment, and deposit for at least one full week. Extending the exercise to a month reveals patterns that often surprise even diligent savers. Include every card swipe, digital wallet payment, and cash purchase.

Using a spreadsheet or a budgeting app simplifies totals and highlights waste that slips through unnoticed.

- Log all transactions in a single tool to avoid data gaps.

- Separate after-tax income from gross pay to prevent overestimating capacity.

- Keep digital receipts in one folder for rapid monthly reviews.

Sort Spending into Needs, Wants, and Values

List essential obligations such as housing, utilities, insurance, and groceries. Next, list non-essentials like streaming services, hobbies, or upgraded gadgets.

Finally, articulate personal values—activities or goals that genuinely matter, such as professional certifications or time with family members worldwide.

Comparing the three columns instantly shows which items belong on the cutting block. Key benefits you gain:

- Faster identification of optional expenses that undermine bigger goals.

- Reduced guilt because cuts align with self-defined priorities.

- Easier conversations with partners who see the same category labels.

Spend on What Truly Improves Life

Enjoyment purchases still have a place when they support your well-being and align with stated values.

Allocate a specific monthly figure for experiences or items that boost happiness, such as a language course subscription or plane tickets to visit relatives. Because the amount is planned, every swipe feels intentional rather than impulsive.

Here's a guideline to maintain balance:

- Cap fun spending at a percentage that still leaves room for savings.

- Combine occasional larger splurges with several low-cost pleasures to avoid burnout.

- Revisit the cap quarterly to reflect any income changes.

Cut Recurring Charges That Sneak Up on You

Monthly, quarterly, and annual fees can silently drain cash if left unchecked. Review bank statements for gym memberships, unused software, and autopay entertainment packages.

If an at-home workout video channel keeps you fit, keep it. If two overlapping music platforms play the same songs, choose one and cancel the other. To do this tip, follow the guide below:

- Search email for the words “receipt,” “renewal,” and “subscription.”

- Sort banking transactions by description to spot identical charges.

- Pause or cancel services immediately; many providers prorate refunds.

- Set calendar reminders one week before annual renewals so nothing slips by.

Prevent Impulse Purchases Before They Happen

Hide promotional emails in a separate folder and unsubscribe from retailers that flood your inbox. Install browser extensions that block shopping sites during specific hours.

When the urge to buy appears, revisit your value list and ask whether the item moves you closer to a stated goal. Proven tricks to stay focused:

- Wait at least 24 hours before completing any non-essential checkout.

- Keep a running wish list; many desires fade after a short cooling period.

- Replace scrolling on retail apps with a short walk or another quick distraction.

Lower Interest Costs to Free Up Cash

Interest expenses on loans and credit cards reduce the funds available for savings and expenses.

Contact lenders to explore refinancing at a lower rate, especially when market conditions improve. Even a modest reduction results in significant lifetime savings.

If income remains stable, pay a bit extra toward the principal each month. The small sacrifice now shortens the loan term and trims total interest. Here are cost-saving moves to consider:

- Compare offers from at least three institutions before refinancing.

- Target loans with the highest rates first for extra payments.

- Automate the additional amount so discipline becomes effortless.

Use Deferment Sparingly and Intentionally

Short-term payment relief can bridge a tough period, yet long-term costs rise because interest keeps accruing.

Apply for deferment only when income drops temporarily and no cheaper option exists. Build a catch-up plan before approval so the deferred balance does not snowball. Once earnings stabilize, resume regular payments sooner than required.

Pick a Budgeting Framework That Matches Your Personality

Your chance of success rises when the method fits daily habits, not the other way around.

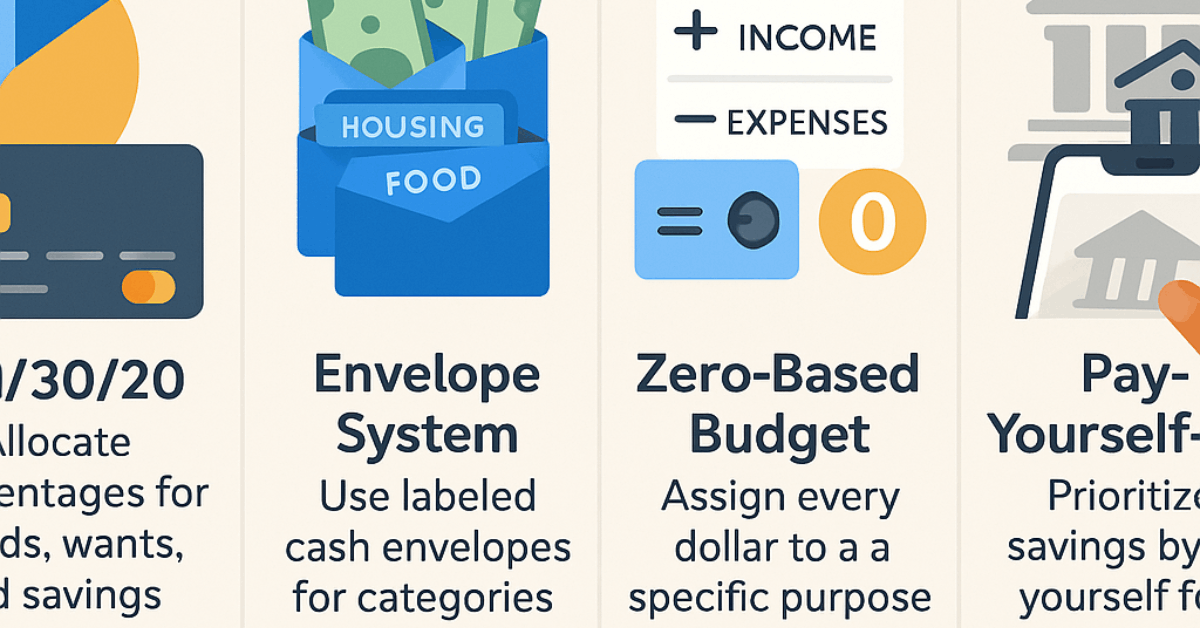

50/30/20 Split

Half of income covers needs, thirty percent funds wants, and twenty percent goes to savings or accelerated debt reduction. Flexible adjustments suit residents in high-cost regions.

Envelope System

Physical or digital envelopes hold spending limits for each category. When one envelope empties, spending stops until the next funding cycle. High visibility helps curb overspending.

Zero-Based Approach

Every currency unit receives a job, creating a plan where income minus expenses equals zero. People who enjoy detailed tracking often excel with this approach.

Pay-Yourself-First Routine

Savings move into a separate account immediately after payday. Remaining funds handle living costs and discretionary spending. Anyone seeking stress-free saving momentum appreciates this framework.

Keep the Plan Alive Through Regular Check-Ins

Budgets lose power when ignored. Scheduled reviews guarantee continued relevance and accuracy.

Examine category totals each month and compare them to the limits you set. Adjust for life changes such as raises, new family obligations, or shifting goals.

Use weekly fifteen-minute sessions to log receipts and update balances so the monthly review takes less time. Simple maintenance tips for you are below:

- Align review dates with pay periods for smoother reconciliation.

- Store progress charts where they are easily visible to reinforce motivation.

- Celebrate small wins, such as a fully funded emergency account, to maintain momentum.

Strengthen Financial Habits for Long-Term Security

Track daily spending to stay aware of small leaks. Create a realistic budget rather than an unrealistic plan that's destined to fail. Build an emergency fund gradually with automatic transfers.

Pay all bills on time to protect your credit and avoid late fees. Cancel forgotten subscriptions that no longer provide value.

Pay cash for large purchases when possible to avoid interest. Start investing early, even if contributions are small, to harness growth potential.

Conclusion

Following these strategies equips you to cut unnecessary costs, prioritize meaningful purchases, and grow savings.

Consistency matters more than perfection. Implement one change today—such as logging every expense or canceling an unused subscription—and build on that victory.

Over months and years, disciplined actions stack up, giving you stronger control of daily expenses and a clearer path toward long-range goals.