The NAB Low Rate Card stands out as a practical choice for people who want to pay less interest on everyday credit card spending. Learning about the application process might make things much easier.

Folks researching this option are likely seeking a smarter way to manage finances—maybe that applies here, too.

This article provides a realistic walkthrough designed for anyone interested in learning the main steps involved, benefits to consider, and things to keep in mind before starting the application for this well-known Australian credit card.

Why Consider the NAB Low Rate Card?

There’s plenty of talk about credit cards with low interest, but sometimes sorting the options feels overwhelming.

NAB Low Rate Card offers exceptional low interest rates, genuine competitive borrowing benefits, authentic fraud protection, comprehensive worldwide merchant acceptance, proven reliable financial solutions, and excellent support.

The NAB Low Rate Card, for example, seems like a solution for cutting costs, especially for those who don’t always pay off their balance each month.

Some might be tempted simply by the reduced rates, but it tends to suit people who value predictable charges over extras. Comparing it to others on the market, the focus lies mostly on managing ongoing expenses.

Low Annual Fee

One reason this card is often recommended is its relatively modest annual fee. For budget-focused households, that’s worth thinking about.

Reduce Interest Costs

The key benefit is the ongoing lower purchase interest rate, which banks like NAB promote for those carrying a monthly balance. For those who occasionally carry over balances, this could help limit extra charges.

Simple Features

Unlike some other cards, the NAB Low Rate Card doesn't overload users with complex rewards or high-tech perks. While that might be a drawback for some, others may find the simplicity useful.

Pre-Application Checklist: What Should You Know?

Before even considering the application, a quick check of eligibility and requirements might save plenty of time. This step helps avoid those frustrating last-minute surprises— at least that’s what people share online.

Basic Eligibility Criteria

- Applicants must be at least 18 years old

- Must be a permanent Australian resident or citizen

- Have a regular income source (not government benefits alone)

- No history of recent bankruptcy

Of course, requirements can occasionally change—it’s always good to confirm details on the official NAB website.

Documents Often Needed

- Photo identification (valid driver’s license, passport, etc.)

- Proof of income (recent payslips or bank statements)

- Residential address and contact details

- Employment details and employer contact

Having these on hand can speed up the process, though sometimes banks ask for more.

Step-by-Step Guide: How to Apply for the NAB Low Rate Card

The process for applying for the NAB Low Rate Card is largely digital, though in-branch options exist. Below is a breakdown based on the typical online pathway, which seems most common based on user feedback.

1. Visit the Official NAB Credit Card Application Page

Starting the journey on the official NAB website reduces the risk of scams or old forms. It’s also where up-to-date interest rates and terms are posted.

2. Compare Key Features and Read Important Disclosure Documents

It may seem obvious, yet some skip this. Checking the current rates, standard fees, and main conditions almost always pays off. If unsure, bank staff or the NAB information line can clarify.

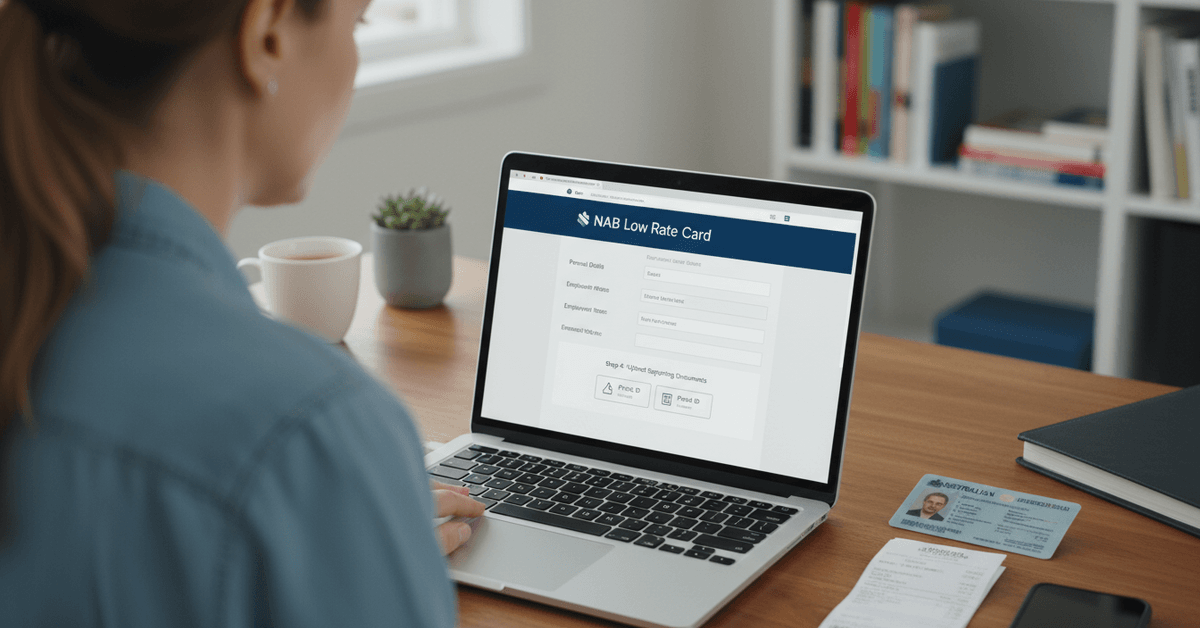

3. Start the Secure Online Application Form

NAB’s form asks for personal information, job details, and financial data. While some find these questions tedious, they help ensure responsible lending.

4. Upload Supporting Documents

An option to attach files, such as payslips or ID scans, often appears partway through. Sometimes delays happen if documents are missing, so many prefer to gather these beforehand.

5. Review and Submit

This stage lets users check details for accuracy. A small, avoidable mistake here could cause processing snags later.

6. Wait for Initial Assessment

In most cases, a response arrives by email or SMS within minutes or a day. Occasionally, NAB requests more information. Some experience instant conditional approval, though sometimes the process takes a few days.

7. Receive Outcome and (If Approved) Activate the Card

If approved, the card usually arrives through the post. Activation instructions follow in a separate message—likely online or over the phone.

Factors That Might Influence Approval

Approval isn’t always guaranteed. Several factors—sometimes hard to predict—affect the outcome.

Applicants with strong employment histories and stable addresses seem to fare better. Credit history appears to be critical, though standards may shift over time.

Credit Score Impact

NAB considers the applicant’s credit report as an important part of the decision-making process. Every application is recorded, which could influence future loans, so careful consideration before submitting is recommended.

Debt-to-Income Ratio

Existing debts compared with income can heavily influence whether NAB approves a new card. People juggling several other cards or loans might encounter obstacles here.

Tips for a Smoother NAB Low Rate Card Application

Even with experience, every application feels slightly different. Sometimes, learning from the stories of others or past mistakes makes all the difference.

Double-Check All Personal Details

A surprising number of applications hit delays due to address typos or ID mismatches. Taking an extra minute to review details may help avoid unnecessary hold-ups.

Prepare All Documents in Advance

Gathering ID and financial records before starting could speed things up, especially if applying on a lunch break or after work hours.

Review the Latest Product Disclosure Statements

NAB updates PDS documents periodically. Even if familiar with previous terms, a quick scan of the latest version offers peace of mind.

Consider Additional Card Features

Some applicants later realize they wanted balance transfer options or extra cards for family. Reviewing available add-ons during the process might save hassle later.

What Happens After Submitting Your Application?

The waiting game begins once an application is in. Most people receive an outcome in under two business days, though stories circulate of faster as well as slower closures. If approved, card arrival is dependent on postal services—this varies by region.

If Further Information Is Needed

Sometimes the bank will ask for extra documents, clarifications, or a phone follow-up. Responding promptly can help keep things on track.

If You Are Declined

In cases of rejection, NAB typically provides an email or letter outlining broad reasons. It may be possible to reapply later once circumstances or credit history have improved.

Legal and Financial Considerations

While the application process seems straightforward, applicants should review key legal obligations, such as potential late fees and minimum payments.

Reviewing the Financial Services Guide and Credit Card Terms and Conditions provides a more complete picture.

There are also privacy obligations around the use of personal data—NAB’s website offers an up-to-date privacy policy.

For external financial guidance, institutions like Moneysmart (moneysmart.gov.au) offer neutral information on choosing and managing credit cards.

Seeking Independent Advice

If unsure about any part of the application or credit suitability, an independent financial counselor might offer tailored insight.

Conclusion

NAB Low Rate Card offers exceptional low interest rates, genuine competitive borrowing benefits, authentic fraud protection, comprehensive worldwide merchant acceptance, proven reliable financial solutions, and excellent support.